¶ General

¶ Biofuels

Biofuels describe fuels produced from biomass (crops, vegetable oils, animal fats, and of waste). Biofuels include carbon-containing liquids such as ethanol, methanol, and biodiesel, as well as carbon-free hydrogen. Biofuels can be used either pure or as a blend. Two biofuels are predominantly used in the world for transport purposes – ethanol and biodiesel.

Biofuels are considered to make a little net contribution to global warming since the carbon dioxide that enters the air during combustion was removed from the air earlier because of plants’ photosynthesis. In practice, the industrial production of biofuels can result in additional emissions of GHG (fossil fuels used during the production process, use of nitrogen fertilizer, indirect land-use change) that may offset the benefits of renewables. Besides, biofuels require large volumes of water and compete for land with other forms of land use, e.g., food production.

The EU Renewable Energy Directive (RED) targeting to increase the share of biofuels in the transport sector, establishes several sustainability criteria for biofuels to be met regarding net GHG savings, biodiversity, and land use. The RED II (2018), establishes that a minimum of 14% biofuels or other renewable fuels for transport shall be used in every Member State by 2030. It also specifies a minimum share of 3,5% of advanced biofuels. These targets were increased to even higher shares of 29% and 5.5% respectively in the the RED III (RED III). Additional information about Biofuels and their potential for a more sustainable transport industry can also be found in our blog articles about these topics (Harnessing biofuels, Carbon Reduction).

Another form of supporting biofuels and less intensive carbon fuels is through the taxation of carbon-intense fuels in the transport sector. The new HDV-road toll initiative is exactly that. The German government agreed upon an HDV street toll system, that is based on the emission class, and thus the carbon intensity of the vehicle. The toll system will slowly start in December of 2023 in Germany and will also initiated on a European scale from March 2024 (read more about this topic in the blog (Emission-based toll system - German).

Source: IPCC, Britannica, European Council, RED, f3 center

¶ Carbon Audit

A carbon audit is referred to a 'carbon footprint' assessment, as a means of measuring and recording the GHG emissions of an organization, activity, project, or product within a defined system boundary.

Carbon audit is generally used for annual climate disclosures, setting and tracking Science-Based targets, analysis of activities and suppliers, product carbon footprints, and more.

In stricter meaning, carbon audit means the process of verification of sustainability reporting by a third party. For example, for the Corporate Sustainability Reporting Directive (CSRD) it will be mandatory for companies to have their sustainability information assured by qualified third parties, consistent with European Commission standards.

Limited CSRD assurance standards are to be adopted in 2026. The suggested proposal is to assess compliance with the reporting rules, a process carried out to provide information, the format provided (digitalization), and compliance with EU Taxonomy reporting requirements. In 2029 the EU council plans to issue reasonable assurance standards. Reasonable assurance is the highest assurance level (as in a financial audit). In a reasonable assurance engagement, the practitioner expresses a conclusion (called “opinion”) as to whether the information is accurate and complete (or: fairly presented), in all material respects, against the (European sustainability) reporting standard.

Source: Accountancy Europe

¶ Carbon Compliance

The term ‘carbon compliance’ or commitment is mostly used with regard to financial schemes to regulate GHG emissions or Carbon Compliance Markets. Governments around the globe have made commitments to limit global warming and reach net zero carbon emissions by 2050 (or sooner) in order to deliver against the targets of the Paris Agreement. Carbon Compliance Markets, also known as Emissions Trading Systems (ETS) have an important role to play in helping to achieve these commitments.

Under these schemes, a limit (cap) is set on the total amount of certain greenhouse gases that can be emitted by the companies covered by the scheme — effectively setting a carbon budget. Currently, there are three major ETS around the world: European Union’s Emissions Trading System (EU); The California Global Warming Solutions Act (USA); The Chinese National Emission Trading System (China).

A more general term ‘sustainability compliance’ means conforming to sustainability standards, legal mandates, regulations, approved plans and permits, and other conditions of approval for activities. is used with regard to measuring the adherence of a company to international or EU-level sustainability regulations, or the ability to a certain threshold for a sustainability indicator.

Source: KPMG, carbon credits

¶ EU Emission Trading Scheme

The EU emissions trading system (EU ETS) is a carbon market operating in all EU countries plus Iceland, Liechtenstein, and Norway. It limits emissions from more than 11,000 heavy energy-using installations such as power stations, industrial plants, or airlines covering around 40% of the EU’s greenhouse gas emissions.

Working on the ′cap and trade′ principle, the EU ETS sets a cap on the total amount of greenhouse gas emissions by the system. Within this cap, companies receive or buy emission allowances, which can then be traded with one another as needed. This gives an incentive for companies to reduce emissions and eventually sell allowances. The market-based approach of using these limited EU ETS will automatically increase the price of the certificates, and thus as well the price of carbon emissions. Overall, the EU ETS is a major pillar of EU energy policy and has been found to be an effective tool in reducing emissions cost-effectively. Today not all parts of the transportation industry are already covered under the umbrella of the EU ETS, but this will potentially change as part of the implementation of the EU Green Deal.

EU ETS is to be extended to:

- Maritime sector from 2023 to 2025; 100% of verified emissions will be surrendered as of 2027;

- Aviation sector: free emission allowances are to be phased out by 2027;

- Road and building sector: commencement date is to be aligned between the EU council and EU parliament.

Source: European Commission, KPMG

¶ Operational boundaries

An operational boundary defines the scope of direct and indirect emissions for operations that fall within a company’s established organizational boundary to help a company better manage the full spectrum of GHG risks and opportunities that exist along its value chain.

Direct GHG emissions are emissions from sources that are owned or controlled by the company, while indirect are the consequence of the activities of the company but occur at sources controlled by another company.

What is classified as direct and indirect emissions is dependent on the consolidation approach (equity share or financial control) selected for setting the organizational boundary. A company may decide not to include emissions from the entity over which it doesn’t have financial control or include it to the extent of equity share. After the organizational boundary is set, the operational boundary (scope 1, scope 2, scope 3) is fixed on the corporate level.

For complex organizations and supply chains, organizational and operational boundaries are important parameters to avoid double counting of GHG emissions. Especially relevant for offsetting schemes.

Source: GHG protocol

¶ Paris Agreement and European Green Deal

The Paris Agreement (PA) is the first-ever universal, legally binding global treaty on climate change. It was adopted by 196 parties at the 21st annual Conference of Parties (COP21), the annual meeting of all nations forming the United Nations Framework on Climate Change in 2015. Its goal is to limit global warming to well below 2°C above pre-industrial times with a goal of not exceeding 1.5°C.

The legal aspect of PA is binding parties to communicate their Nationally Determined Contributions (NDC), voluntarily defined. As of October 2022, the combined climate pledges of 193 Parties under the PA could result in 2.5 degrees above pre-industrial times by 2100. The European Green Deal is a similar trans-country climate initiative on the European continent. The main goal is to reduce GHG emissions by 55% by 2030 and to be a climate-neutral continent by 2050 (European Green Deal). For the transport sector, the European Green Deal specifies reducing GHG emissions by 90% by 2050, using at least 40% sustainable fuels in aviation, cutting at least 40% of shipping emissions, and shifting 50% from road to rail for medium distances (ECEEE).

Source: United Nations (1), United Nations (2)

¶ Sustainability

Sustainability, Sustainable Development refers to meeting the needs of the present generation without compromising the needs of future generations. The concept of sustainability is based on three pillars: environmental, economic, and social sustainability. A great number of sustainability challenges exist within this triangle. To help businesses be transparent about their impact and take responsibility, a number of standards and initiatives were developed. The Global Reporting Initiative (GRI) is a globally recognized institution for setting standards on comparable and comprehensive sustainability reporting.

¶ Sustainable Aviation Fuel (SAF)

Sustainable aviation fuel (SAF) is renewable or waste-derived drop-in aviation fuel that meets sustainability criteria. SAF is produced from sustainable, renewable feedstocks such as used cooking oils, forestry, and agricultural residues, municipal solid waste, and captured CO2. SAF is considered the most viable factor for aviation decarbonization.

The chemical and physical characteristics of SAF are almost identical to conventional jet fuel and can be mixed with the latter to varying degrees, use the same supply infrastructure, and do not require the adaptation of aircraft or engines.

Currently, airlines may use any SAF that meets the technical certification criteria, but no uniform sustainability standard exists. The International Air Transport Association (IATA) suggests that SAF should meet the following criteria: lifecycle carbon emissions reduction, limited fresh-water requirements, no competition with needed food production (first-generation biofuels), and no deforestation.

The fact of using carbon-neutral SAF doesn’t automatically make the flight carbon-neutral. Depending on the emissions calculation methodology (see, for example, GLEC) the full flight cycle can be included: taxiing, take-off, as well as any other movement related to freight loading and unloading, etc.

The price for SAF is two to five times higher than the standard jet fuel and represents < 0.1% of total demand. Within ´fit for 55 package’ there exists a ReFuelEU Aviation initiative that proposes to oblige fuel suppliers to distribute SAF, with an increasing share of SAF over time. ReFuelEU also seeks to define the parameters of sustainable aviation fuel by law.

Source: IATA, European Parliament, KPMG, World Economic Forum

¶ Sustainable Development Goals (SDG)

In 2015, the United Nations member states adopted 17 Sustainable Development Goals (SDG) as a universal call to action to end poverty, protect the planet and ensure peace and prosperity worldwide.

The goals recognize the interconnection and equal importance of environmental, economic, and social sustainability. That means that ending poverty and other deprivations must go side by side with actions that reduce inequality, improve health and education, and accelerate economic growth while fighting climate change and protecting our oceans and forests.

To convert SDGs into strategic industry activities, United Nations Global Compact Initiative and KPMG developed the SDG industry matrix for 6 business areas, including Transportation, outlining specific ideas for action for each SDG.

Source: United Nations, SDG industry matrix

¶ System boundaries

Depending on reporting or analytical goal, GHG footprint or GHG emissions inventory can be defined within different system boundaries: product, project, function, corporation, region, etc.

The table below shows the differences in system boundaries for corporate, product, and transportation services GHG footprint. For each accounting level, the major standards and calculation guidance are outlined:

| Corporate Carbon Footprint | Product Carbon Footprint | Transport Services Footprint | |

| System boundaries | organizational boundaries, and associated emissions, categorizing them as direct and indirect emissions, and scopes (1-3) | GHG inventory shall include all attributional processes, irrespective of whether own or 3d party processes | GLEC: a freight movement begins with the hand-over of the consignment to the party transporting the shipment and ends with the hand-over of the shipment to the consignee |

| Standards and norms |

|

|

|

Source: GHG Protocol (1), GHG Protocol (2), GLEC framework, ISO, PAS 2050

¶ Emissions

¶ Additionality

The Greenhouse Gas Protocol defines additionality as a criterion for assessing whether a project has resulted in GHG emission reductions or removals in addition to what would have occurred in the project’s absence.

It is an important aspect to consider in compensation strategies to avoid greenwashing.

Source: GHG Institute

¶ Avoided emissions

There is considerable interest among companies in claiming that their products or services can help avoid GHG emissions compared to other products or services with the equivalent function.

Comparative impacts of products with equivalent functions can be estimated using either attributional or consequential accounting approaches.

The attributional approach compares emissions of a reference, alternative product, with a company’s product.

The consequential approach compares the referenced system-wide change in emissions from a given decision or intervention, in response to, for example, changes in production technology, public policy, or consumer behavior.

|

Attributional approach Comparative GHG impact = Life Cycle Emissions of Referenced Product - Life Cycle Emissions of Assessed Product |

Consequential approach Comparative GHG Impact (Policy) = Emissions in baseline scenario - Emissions in policy scenario |

Calculated positive impacts are considered avoided emissions. Comparative emissions assessments should by no means replace accounting scope 1,2,3 emissions.

Source: GHG Protocol

¶ Black carbon

Black carbon is the most strongly light-absorbing component of particulate matter. It is formed by the incomplete combustion of fossil fuels and biomass and is emitted in the form of fine particles. The climatic influences of black carbon are its strong absorption of light, both directly and indirectly through the reduction of snow and ice reflectivity, leading to increased temperatures and accelerated ice and snow melting. After carbon dioxide, black carbon has the second biggest impact on climate forcing in the atmosphere. Black carbon typically remains in the atmosphere only for days to weeks, until it returns to the earth’s surface through the rain.

For the Logistics Sector, the Black Carbon Methodology was developed in 2017 as an annex to the GLEC Framework.

Sources: EPA, CCA Coalition

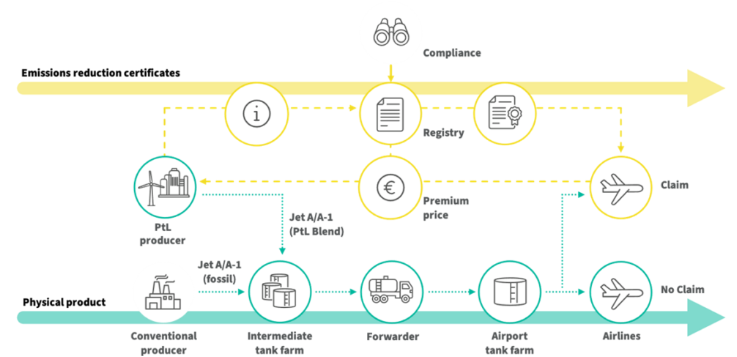

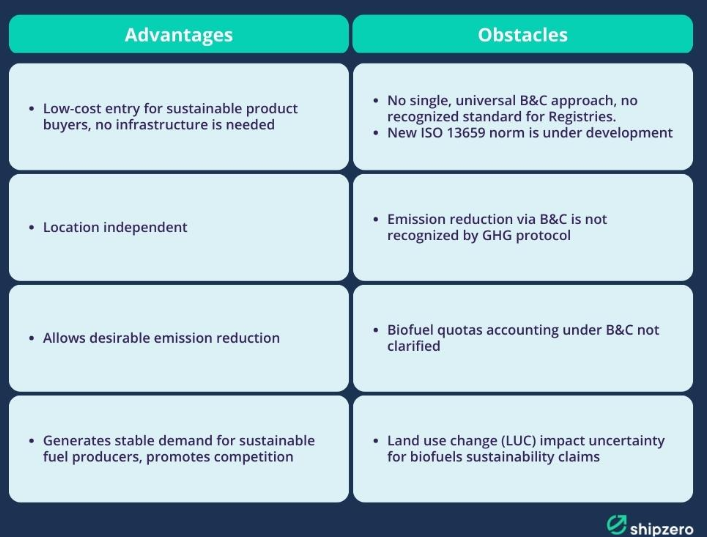

¶ Book & Claim

Book & Claim (B&C) is a method for offsetting and insetting emissions by claiming carbon emission reductions from a specific service without using or owning that service in exchange for a premium. The most known example is the claim of reduced emissions from sustainable fuels.

The emissions of the biofuel and the biofuel itself are separated into the physical component (the fuel) and the non-physical component, the (reduced) emissions certificate, and sold separately. That means that it is possible for a company to “book” an amount of biofuels in one location, while another can “claim” the emissions savings (thus the emissions certificate) in another location. The claiming of the reduced emissions in another location normally comes with a premium price for the more sustainable fuel and can only be claimed once. However, the net CO2e difference in the atmosphere is the same no matter where the emissions savings are being claimed.

This method has the advantage of enabling location and infrastructure-independent emissions reduction possibilities, this reduces the entry barriers for many companies. However, the novelty of this process currently means that no universal standard for B&C exists.

More information about this new method and its development can be found in our blog post about B&C (Book & Claim).

¶ Buyer’s principle

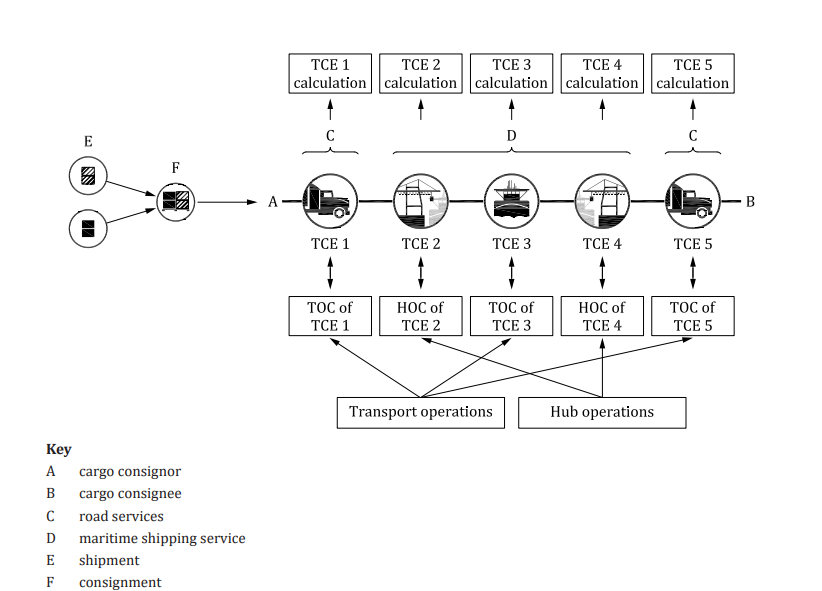

GLEC framework states that emission reporting data should be tailored to customer service (B2B principle), i.e., tied to a contract and associated invoice. Service provided to a customer, thus, considered as a minimum level of reporting by a company (logistics service provider, carrier).

The allocation method must be transparent and standardizable to avoid any discussions about the interpretation of the figures. To exclude double counting, Incoterms® rules (determine the responsibility distribution for selection of transportation mode and route, shipment characteristics) can serve as a basic rule to emissions allocation.

A freight movement begins with the handover of the consignment to the party transporting the shipment and ends with the handover of the shipment to the consignee. Similarly, freight emissions from transport routes with single or several points of loading and unloading can be allocated to individual consignments. For joint consignments, the weight factor is applied. For logistics sites that are jointly operated, the allocation of emissions should be based on the throughput tonnage related to a buyer.

EN 16258 emissions allocation principles are to be updated in ISO 14083.

Source: GLEC framework

¶ Carbon Abatement

Refers to reducing the degree or intensity of greenhouse-gas emissions, via both, reducing carbon emissions or reducing carbon already in the atmosphere through carbon sequestration.

Source: UNFCC, International Energy Agency

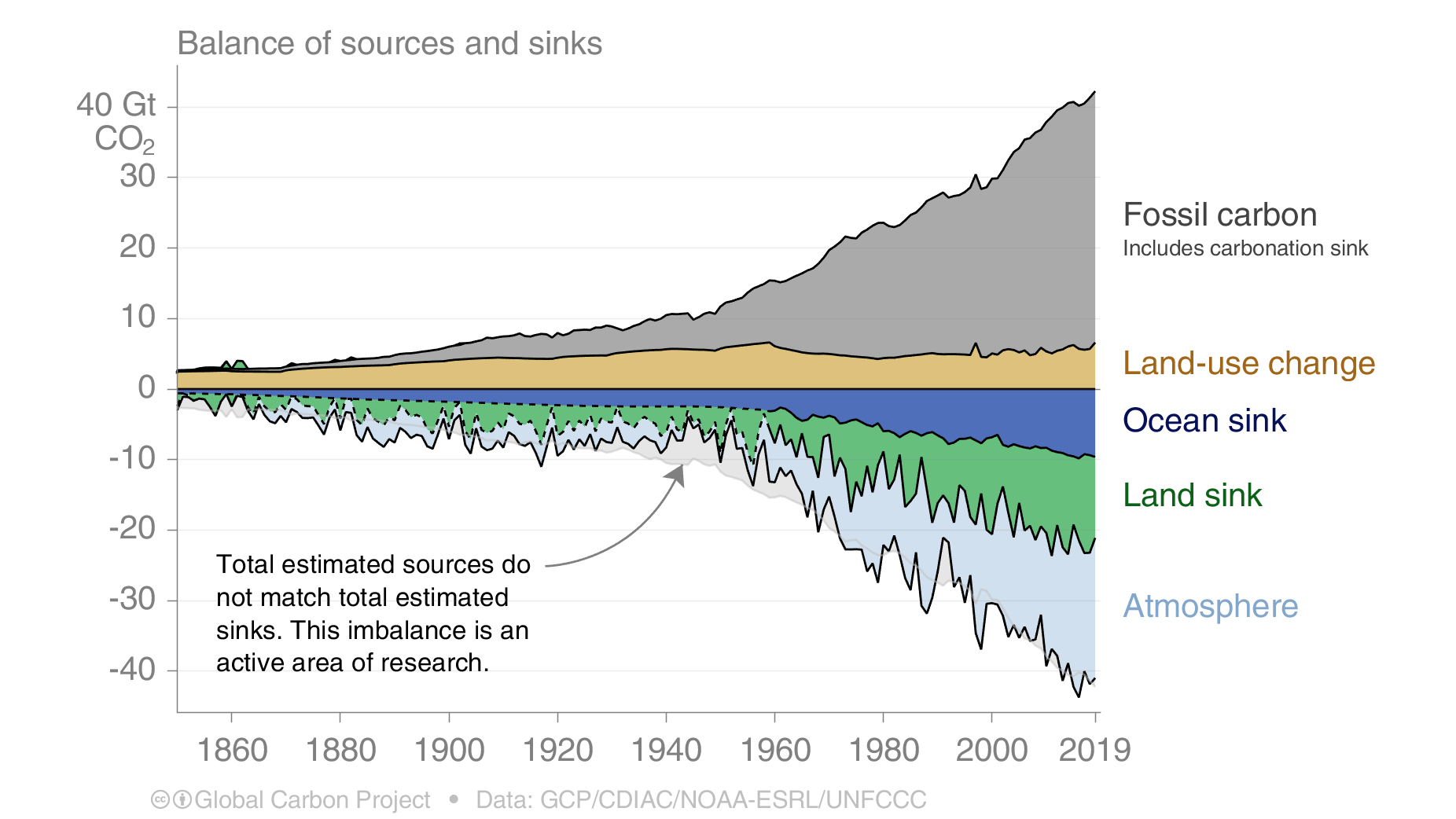

¶ Carbon dioxide (CO2)

Carbon dioxide (CO2) is the primary greenhouse gas emitted through human activities. Although it is naturally present in the atmosphere as part of the earth’s carbon cycle, human activities alter the carbon cycle by adding more CO2 to the atmosphere while decreasing the number of natural sinks, like forests or soils, that remove and store CO2.

Source: EPA

¶ Carbon dioxide equivalent (CO2e)

A common way to compare greenhouse gases is the carbon dioxide equivalent (CO2e). It is a metric based on each greenhouse gas’ global-warming potential (GWP) that converts amounts of other gases to the equivalent amount of carbon dioxide with the same GWP. For example, methane has a GWP of 25, meaning that its GWP is 25 times as high as that of CO2. In comparison, nitrous oxide has a GWP of 298 and sulfur oxides even of 14,800 to 22,800.

Source: European Commission, Brander & Davis (2012)

¶ Carbon footprint

The carbon footprint is a measure of the total amount of emissions that are caused by an activity or organization or are accumulated over the life stages of a product. The measurement includes all direct and indirect emissions (Scope 1-3) to account for completeness and accuracy. Carbon footprint considers non-CO2 emissions as well (e.g. CH4, N2O) of which the global warming potentials (GWPs) are much higher than that of CO2. Similarly, the terms corporate footprint, product footprint, and transport footprint have been established.

The following methods give companies guidance on Carbon Footprint calculation: PAS 2050, GHG Protocol & ISO 14064 (organizational and project level), and ISO 14067 (product level).

Source: Wiedmann, Minx (2007)

¶ Carbon insetting

Opposite to carbon offsetting, carbon insetting suggests reducing emissions within a firm’s own supply chain Scope 3 emissions.

While no standardization of the term exists, several approaches to defining carbon insetting are being considered.

SBTI Corporate net-zero standard suggests the conservative view, where three types of emissions reduction interventions are considered:

- That are wholly contained within a Scope 3 supply chain boundary of a company;

- Or is a project partially within their Scope 3 supply chain boundary (spanning their supply chain and other companies’ supply chains);

- Or is a project adjacent to a supply chain boundary.

An accounting approach has not yet been settled in the GHG Protocol.

For the transport industry, Smart Freight Center, highlighting the high decarbonization barriers (supply chain size complexity, high costs, restricted access to sustainable options) suggest a flexible ‘book and claim’ approach, allowing shippers or forwarders to share freight emissions costs. A shipper or forwarder aiming to reduce emissions does not need to have their freight physically transported by a reduced emission asset, but paying a premium can report a reduced transportation footprint for their freight.

The physical examples of carbon insetting in logistics are sustainable fuels, engine retrofits, fleet renewals/equipment decommissioning, and shipping/logistics efficiency.

Source: SBT, Smart Freight Center

¶ Carbon intensity

Carbon intensity, also emissions intensity, is the level of CO2 emissions per unit of a specific activity. It is used to compare the environmental impact of different activities or of the same activity in different execution variations. A well-known example is how many grams of CO2 are released to produce a kilowatt hour (kWh) of electricity using coal, gas, or wind.

To analyze the carbon intensities of the supply chain, all greenhouse gases emitted are referred to the transported volume in tonne-kilometre or twenty-foot-equivalent units (TEU).

Source: Hoffmann, Busch (2008)

¶ Carbon offsetting and compensation

Carbon offsetting (or compensation) means paying a third party to cut or absorb an equivalent amount of emissions from a dedicated activity (e.g., transport) that set emissions-free. It is important to precisely measure or calculate the amount of emissions that is compensated for.

Typical carbon offsetting projects are investments in reforestation or renewable energies and are often located in developing countries. Carbon offsetting is an important part of many organizations’ sustainability programs but is also becoming increasingly popular for individuals, e.g., to compensate for personal activities such as flight travel.

Owing to their indirect nature, many types of offset are difficult to verify. According to GLEC, while carbon offsets may be purchased as part of a company’s overall corporate social responsibility (CSR) strategy, they should not be deducted from a company’s reported total emissions.

Source: Britannica, GLEC framework

¶ Carbon sequestration

Carbon sequestration is the long-term storage of carbon in plants, soils, geologic formations, and the ocean. Carbon sequestration occurs both naturally and as a result of anthropogenic activities, and typically refers to the storage of carbon that has the immediate potential to become carbon dioxide gas.

In response to climate change concerns and the insufficiency of current efforts on emission reduction, considerable interest has been drawn to carbon sequestration through changes in land use and forestry, and through geoengineering techniques such as carbon capture and storage.

For accounting purposes, a new GHG Protocol guidance for land sector activities and CO2 removals in corporate greenhouse gas inventories is to be published in 2023.

A proposal on carbon removal certification is being prepared by the European Commission.

Source: Britannica, GHG Protocol, European Commission

¶ CO2 price

A CO2 price is a price that companies have to pay for the emission of CO2, either in form of a carbon tax or tradeable emission certificates. Carbon pricing is seen as the most efficient way for nations to reduce greenhouse gas emissions and is applied European-wide for several industries through the EU emissions trading system (ETS). Germany and several other countries launched additional national pricing mechanisms for the transportation sector with a fixed price that gradually increases over time.

Source: Worldbank

¶ Decarbonization

Decarbonization means reducing, and ultimately eliminating CO2 from recurring activities that are powered or enabled by burning fossil fuels. The goal is to decrease the carbon intensity to net zero. This requires a switch to fully renewable energy sources or active capturing of the equivalent amount of emissions from the atmosphere.

Source: ISE

¶ Emission factors

An emission factor is a representative value intended to estimate the amount of pollutant released to the atmosphere based on an underlying activity. Emission factors are usually expressed as the weight of the pollutant divided by a unit weight, distance, volume, or duration of the related activity (e.g., kg of CO2 emitted per kWh of natural gas). In most cases, emission factors are averages of all available data of sufficient quality and are assumed to represent long-term averages for all facilities in the source category. Widely used transport emission factors are released by the GLEC Framework and Clean Cargo Working Group.

Source: EPA

¶ Estimation uncertainty

Similar to financial statements about complex systems, also carbon accounting underlies an estimation uncertainty. This uncertainty is comparably even higher due to the fact that a company rarely has full information about all greenhouse gas emitting processes along their transport chains.

Estimates can therefore be oversimplified or wrong, given that assumptions made are incorrect. However, as not all agents in a network of transport operators have the same scope and level of detail in information, deviating results for the emission footprint based on different input information is a rather common phenomenon.

Three things are important to consider when dealing with estimation uncertainty:

- Sufficient and appropriate evidence for making assumptions, e.g. not neglecting data assets that would create more granular insights

- Transparent documentation of estimation assumptions, and consistency in their application (e.g. following an internationally recognized standard)

- Allowing verification from independent parties

Source: ACCA

¶ Fluorinated gases (HFC/HFO)

Hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulfur hexafluoride (SF6), and nitrogen trifluoride (HFCs) are synthetic, powerful greenhouse gases that are emitted from a variety of industrial processes. Unlike most other greenhouse gases, fluorinated gases have no natural source but exclusively come from human-related activities.

The vast majority is emitted through their use as refrigerants, for example in air conditioning systems in vehicles and buildings. Fluorinated gases have very high global warming potentials of up to 22,800 and are the most potent and longest-lasting type of greenhouse gases emitted by human activities. Their reduction especially in cold chain transports (food, pharmaceuticals, etc.) is very important.

Source: EFCTC, European Commission

¶ Fugitive emissions

Fugitive emissions are emissions from the unintentional or intentional release of greenhouse gases (GHG) to the atmosphere. Releases can be accidental, caused by equipment leaks, or they can be intentional venting or discharging of GHGs: methane emissions from coal mines and venting; hydrofluorocarbon (HFC) emissions during the use of refrigeration and air conditioning equipment; and methane leakages from gas transport.

For the logistics sector, fugitive emissions from air-conditioning, refrigerants and LNG transportation and LNG fueled trucks and ships. Refrigerant usage in mobile or stationary equipment causes the release of hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulphurhexafluoride (SF6), may occur during the manufacturing process, from leakage during equipment usage, or from refrigerant disposal at the end of the life of the equipment.

Fugitive methane emissions are a concern for owners and operators of LNG-fueled trucks and ships. It can escape:

1) during the processing of LNG;

2) any unburned methane escapes from the engine into the atmosphere, and

3) for safety reasons, the gas may also need to be vented to avoid creating a hazardous environment.

EPA provides detailed guidance on different methods for fugitive emissions calculation. GHG protocol specifies GHG scope for these emissions for different industrial sectors.

Source: GHG Protocol, EPA

¶ GHG registry

A GHG registry is a database for collecting, verifying, and tracking emissions data from emitters, such as facilities or companies. Registries can serve a variety of objectives, be voluntary or mandatory, be administered by governments or industry groups. Voluntary registries collect data from businesses and organizations seeking to demonstrate emissions reduction efforts. Mandatory registries primarily serve the regulatory purpose of ensuring compliance with regulatory programs.

In 2012, EU Emissions Trading System (ETS) operations were centralised into a single EU registry operated by the European Commission. It is an online database accounts for stationary installations (transferred from the national registries used before 2012) and for aircraft operators (included in the EU ETS since January 2012).

The Registry records:

- National implementation measures

- Accounts of companies or individuals holding such allowances

- Transfers of allowances ("transactions") performed by account holders

- Annual verified CO2 emissions from installations and aircraft operators

Annual reconciliation of allowances and verified emissions, where each company must have surrendered enough allowances to cover all its verified emissions

Source: WRI, GHG Protocol, European Commission

¶

Greenhouse gases

A greenhouse gas (GHG) is a gas that retains heat, causing the greenhouse effect. The primary greenhouse gases in Earth's atmosphere are water vapor (H2O), carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), and ozone (O3). The Earth's natural GHG effect allows an average surface temperature at 15 °C. Excessed GHG emissions, mainly caused by the unprecedented intensity of fossil fuel burning and land use, lead to global warming.

Seven gases were outlined by Kyoto Protocol (1997) to curb global warming: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), and fluorinated gases (HFCs, PFCs, SF6, and NF3).

{kind=link}

¶ Logistics site emissions

Logistics sites are facilities that connect transport legs or are the starting or end points of a transport chain. This includes terminals, ports, airports, warehouses, cross-docking sites, distribution centers, and more. It is estimated that warehouse and sorting facilities alone can comprise up to 13% of supply chain emissions.

The boundary for emissions from logistics sites begins when the consignment is unloaded from the inbound vehicle or vessel and ends when the goods are either handed over to the recipient or reloaded onto the outbound vehicle or vessel.

IPCC recommends two following methodologies: Guidance for Greenhouse Gas Emissions Accounting at Logistics Sites, and Guidance for Greenhouse Gas Emission Footprinting for Container Terminals. GLEC framework aligns with these two.

ISO 14083 bridges the allocation of shipment-level emissions and recommends a joint consideration of cargo movement along with storage and transshipment. The allocation of logistics site emissions to individual shipping units is usually done on a throughput basis of units / and or weights.

Source: GLEC framework

¶ Methane

Methane (CH4) accounts for around 10% of all greenhouse gas emissions from human activity. Human activities emitting methane include the raising of livestock, leaks from natural gas systems, or waste management in the form of landfills. Its comparative impact on global warming is 25 times bigger than CO2.

Source: EPA

¶ Negative emissions

The term negative emissions is used by climate scientists of the Intergovernmental Panel on Climate Change (IPCC) as practices or technologies that remove CO2 from the atmosphere. Two main types of negative emissions are distinguished: enhancing existing natural processes that remove CO2 from the atmosphere (e.g., afforestation and reforestation or the increase of other ‘carbon sinks’) or using technological solutions that capture CO2 directly from the ambient air. Commonly used synonyms of negative emissions are carbon dioxide removal or greenhouse gas removal. The term removal can be confusing in this context as only the chemical state of carbon-dioxide molecules changes.

Source: IPCC

¶ Net zero emissions

The term net zero emissions refers to the achievement of a balance between CO2 sources and sinks, meaning that the amount of CO2 released into the atmosphere must equal the amount that is removed. The underlying implication of this ‘carbon neutrality’ is that the concentration of CO2 in the atmosphere would slowly decline until CO2 emissions from human-related activities can be redistributed and absorbed by the land biosphere and the oceans. This would result in a near-constant global temperature over many centuries and hence an end to global warming.

Source: IPCC

¶ Nitrogen oxides (NOx)

Nitrogen oxides refer to a binary compound of nitrogen and oxygen or a mixture of such compounds. In the context of environmental damage, nitrous oxide (N2O) is known for having a global-warming potential that is almost 300 times greater than that of CO2. It makes up about 6% of all greenhouse gas emissions from human activities, mostly emitted through agricultural soil management activities. The greatest problem with N2O is that its molecules stay in the atmosphere for an average of 114 years before being destroyed through chemical reactions or removed by a sink.

For the maritime shipping industry, the International Maritime Organization (IMO) introduced NOx Emission Control Areas (NECAs) in the North Sea and Baltic Sea. These will apply to vessels built after the start of 2021 and reduce the amount of NOx emitted by operations of the vessels to thresholds determined by the engine's speed.

¶ Rebound effect

Increased efficiencies in the usage of energy, raw material, and water enhance sustainability, but also reduce product, process, or service costs, which can, in turn, raise consumption due to lower selling prices. Hence, original savings are partly or even fully cancelled out due to increasing demand. This phenomenon is known as the rebound effect.

Source: UBA

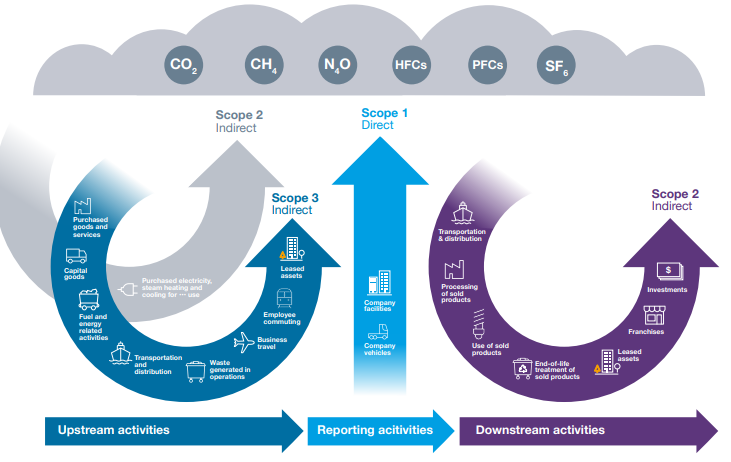

¶ Scope 1, 2, 3

For calculation and reporting purposes, emissions are divided into three parts by the Greenhouse Gas Protocol depending on their source and level of control by an organization

Scope 1 includes all direct greenhouse gas emissions from sources owned or controlled by the organization.

Scope 2 comprises the indirect GHG emissions that result from electricity, steam, and heat purchased and used by the organization.

Scope 3 covers all other indirect GHG emissions resulting from upstream and downstream business activities such as transportation that are not directly owned or controlled by the reporting entity. Scope 3 emissions usually make up the greatest share of the organization’s carbon footprint.

Especially scope 3 emissions are difficult to calculate and allocate correctly due to global supply chain networks with many different stakeholders. Reports from Smart Freight Centre, the Carbon Disclosure Project, and the Science-based target's initiative give practical guidance on how to account for scope 3 emissions.

Sources: Greenhouse Gas Protocol, Smart Freight Centre, Science-based targets

¶ Secondary effects (leakage)

These are GHG emissions changes resulting from the project not captured by the primary effect(s). Secondary effects are typically the small, unintended GHG consequences of a project and include leakage (changes in the availability or quantity of a product or service that results in changes in GHG emissions elsewhere) as well as changes in GHG emissions up- and downstream of the project. If relevant, secondary effects should be incorporated into the calculation of the project reduction. See also fugitive emissions.

Source: GHG Protocol

¶ Stationary combustion emissions

Stationary fuel combustion sources are devices that combust solid, liquid, or gaseous fuel, generally for the purposes of producing electricity, generating steam, or providing useful heat or energy for industrial, commercial, or institutional use, or reducing the volume of waste by removing combustible matter. Stationary fuel combustion sources include but are not limited to, boilers, simple and combined-cycle combustion turbines, engines, incinerators, and process heaters.

Combustion of fuels in stationary (non-transport) combustion sources results in the following greenhouse gas (GHG) emissions: carbon dioxide (CO2), methane (CH4), and nitrous oxide (N2O).

IPCC report (2006) describes the methods and data necessary to estimate emissions from Stationary Combustion and the categories in which these emissions should be reported. Methods are provided for the sectoral approach in three tiers based on:

- Tier 1: fuel combustion from national energy statistics and default emission factors;

- Tier 2: fuel combustion from national energy statistics, together with country-specific emission factors, where possible, derived from national fuel characteristics;

- Tier 3: fuel statistics and data on combustion technologies applied together with technology-specific emission factors; this includes the use of models and facility-level emission data where available.

For the logistics industry, stationary combustion emissions are important when accounting for logistics sites' GHG emissions.

¶ Sulfur oxides (SOx)

Sulfur oxides compounds of sulfur and oxygen molecules and are predominantly found in the form of sulfur dioxide (SO2). It is mostly produced from the combustion of fossil fuels. SO2 concentrations are especially relevant in the maritime shipping industry.

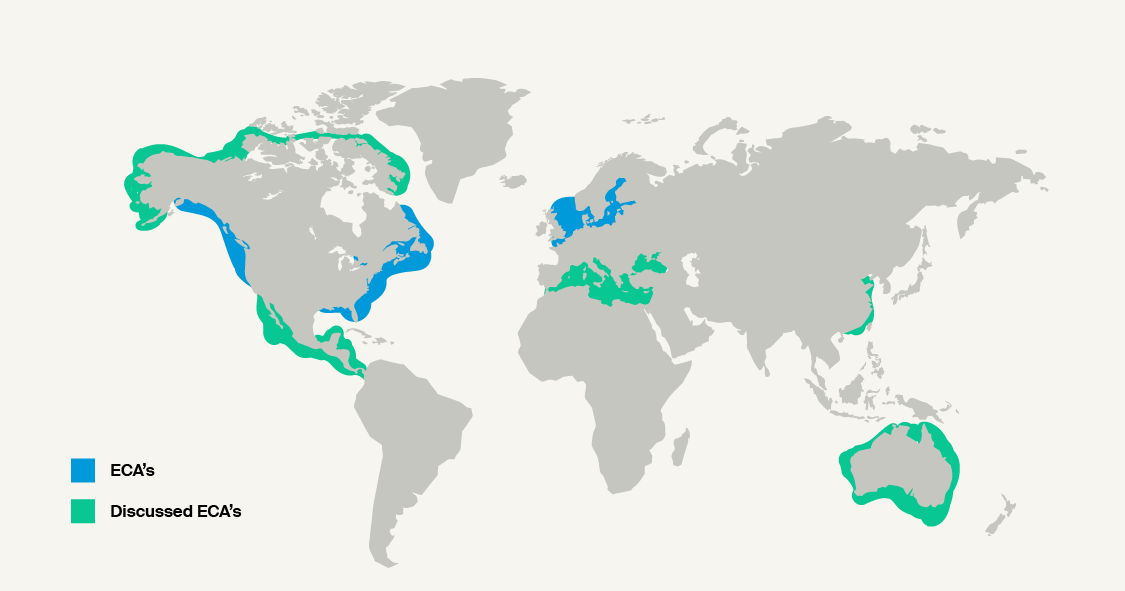

Since 1 January 2020, sulfur emissions from fuel oil used by maritime vessels are regulated to not surpass 0.50% m/m (mass by mass) globally by the International Maritime Organization (IMO). Ships sailing in a Sulphur Emission Control Area (SECA) cannot use fuels with more than 0.1% sulfur.

Source: European Commission, IMO

¶ Transport emissions

Transport emissions refer to all pollutants (greenhouse gases and particulate matter) that are emitted in conjunction with freight and passenger transportation. Transport is the second largest contributor to climate change due to extreme dependency on fossil fuels, and accounts for more than one-quarter of all greenhouse gas emissions in the European Union. Road transport makes up the greatest share with 62% of freight transport emissions, followed by maritime (27%) and aviation (6%). In general, maritime and rail transportation are seen as the greenest modes, while aviation and road transport have higher relative greenhouse gas emissions per distance traveled.

GLEC framework provides one of the most recent and sophisticated methodologies for calculating and reporting logistics emissions.

Sources: EEA (1), EEA (2), GLEC

¶ Value chain emissions

Value chain emissions (also known as scope 3 emissions) are the emissions that occur either upstream (i.e., in the supply chain) or downstream (i.e., during product use and disposal) of the company itself. For many companies, value chain emissions make up to 90% of their total emissions, which makes it crucial for these emissions to be taken into account when setting reduction targets.

Guidance for the value chain emissions accounting and reporting is provided by GHG protocol and ISO 14064.

Source: GHG Protocol (1), GHG Protocol (2), ISO

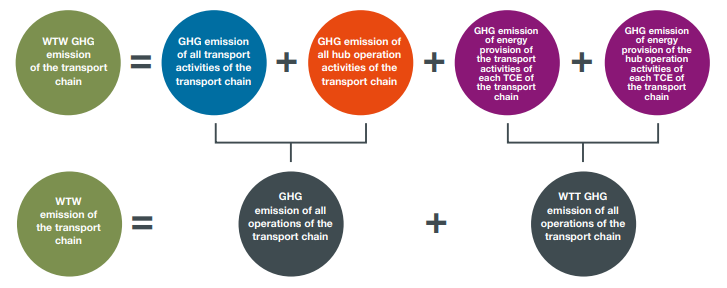

¶ Well-to-wheel, well-to-tank, tank-to-wheel

To capture the climate impact of the full fuel life cycle, well-to-wheel (WTW) emission factors are used. WTW factors are comprised of two categories: well-to-tank (WTT) and tank-to-wheel (TTW) (see figure).

Also referred to as direct and indirect emissions, differentiates between the origin of the energy used for propulsion in transport activities.

Well-to-tank (WTT): Emissions caused by the provisioning of the primary propulsion energy. Emissions caused by transforming primary energy (sunlight, biomass, oil, coal, nuclear, etc.) to consumable energy for vessels or vehicles (diesel, kerosine, hydrogen). Includes extraction, processing, storage, and delivery phases up until the point of use (the tank). These emissions are also referred to as “energy provision emissions”.

Tank-to-wheel (TTW): Emissions caused by converting the vehicle or vessel fuel to propulsion, e.g., burning diesel. These emissions are also known as “transport operation activity emissions” and also include the emissions caused by hubs.

Well-to-wheel (WTW): are emissions from the full fuel life cycle and should be equivalent to the sum of WTT and TTW. It allows the comparability of fossil and renewable fuels, e.g., considering the origin of electricity for battery-electric-vehicles to reflect the share of coal or fossil gas on the local electricity grid.

Modern energy carrier life-cycle analyses also include the emissions that are caused and needed for the hub operations (next to the transport operations). These emissions are captured in the WTW GHG emissions of the transport chain, which includes both the emissions caused by vehicles and hubs, with the associated WTT and TWW components of each activity.

Source: European Commission

¶ Emissions Calculation Standards and Frameworks

¶ DIN SPEC 91224

DIN SPEC 91224 focuses on road transport that lies within the direct or indirect area of responsibility of a company. It supports the practical implementation of inter-company emission balancing in transport on the basis of existing norms, standards, and guidelines with the aim of increasing the control capability of individual actors in the supply chain.

For this purpose, the use of company-specific data instead of generic default data in standardized formats is intended. This, in turn, enables the standardization of inter-company information exchange between all players in the transport chain. The application of DIN SPEC 91224 requires the implementation of EN 16258.

Source: Beuth

¶ GLEC framework(s)

As of today, the GLEC (Global Logistics Emissions Council) framework is one of the most recent and sophisticated methodologies for calculating and reporting logistics emissions. It is globally applicable and includes multi-modal supply chain calculation methods that can be implemented by shippers, carriers, and logistics service providers.

The GLEC framework is in accordance with the Greenhouse Gas Protocol, EN 16258, ISO 14083, as well as the Carbon Disclosure Project. It was published by the Smart Freight Centre and was developed by a voluntary partnership of companies, industry associations, and green freight programs, on the initiative of the Smart Freight Centre. The GLEC framework is regularly updated to reflect state-of-the-art developments. The GLEC as a supportive document to the ISO14083 has the main task of serving the industry as a guideline on how to implement it.

The latest GLEC version (GLEC 3.0), which was just published in September 2023 is fully aligned with the ISO 14083. Next to supporting the implementation of the ISO14083, the GLEC 3.0, also updated various default values of fuel emissions, load factors or intensities of the ISO and aligned the terminology that was used in the earlier GLEC 2.0 version.

The GLEC 3.0 helps companies to track, monitor, and measure their carbon footprint thus providing the opportunity for decarbonization.

Source: Smart Freight Centre

¶

Greenhouse Gas Protocol

The Greenhouse Gas (GHG) Protocol provides the world’s most widely used GHG accounting frameworks for measuring and managing GHG emissions from private and public sector operations, value chains, and mitigation actions. The GHG protocol was one of the first global GHG emissions accounting schemes, that was initiated by the World Resource Institute (WRI) and the World Business Council for Sustainable Development (WBCSB) in collaboration with governments, private companies, industry associations and NGOs.

More than 90% of Fortune 500 companies use GHG Protocol directly or indirectly through a program based on GHG Protocol. The GHG Protocol is also involved in the Paris Agreement, by developing standards, tools and training for countries to monitor their climate goals.

Source: Greenhouse Gas Protocol, GHG Protocol

¶ EN 16258

EN 16258 is a European standard that specifies a uniform method for the calculation and declaration of energy consumption and greenhouse gas emissions for transport services in passenger and freight transport. Published in 2012, it specifies general principles, definitions, system boundaries, calculation methods, apportionment rules (allocation), and data recommendations, as well as provides examples of how to apply these principles.

The new ISO 14083 replaced EN 16258 and, thus will be used less nowadays, as both the ISO 14083 and the GLEC 3.0 provide more detail for the calculations and more recent emission factors and default values.

¶ IMO 2020

IMO 2020 is the abbreviation for a global requirement on marine fuels published by the International Maritime Organization (IMO) that came into force in January 2020. It mandates a reduction of Sulphur oxides of 85% for all ships with a maximum Sulphur content of 0.5% in marine fuels globally and thus replaces the former limit of 3.5%. Emission Control Areas (ECAs) demand an even stricter Sulphur content of maximal 0.1%.

Source: IMO

¶ ISO 14001

ISO 14001 is a globally accepted and applied standard for environmental management systems. Organizations of all types and sizes as well as geographical, cultural, and social conditions can get certified.

However, ISO 14001 does not set absolute requirements for environmental performance. Thus, two organizations with similar activities, but different environmental performances can still both meet the requirements set by ISO 14001. ISO 14001 is particularly common in the chemical industry and the handling of hazardous goods.

¶ ISO 14064

ISO 14064 provides guidance for GHG quantification, monitoring, reporting, validation, and verification, both on organizational and project levels. Regulated and voluntary programs such as Emission Trading Schemes and public reporting are supported by this norm.

The standard is divided into three parts:

Part 1 details principles and requirements for organization-level GHG inventories;

Part 2 describes these requirements on the project level;

Part 3 establishes a process to verify GHG inventory reports created via part 1 and part 2 or other GHG quantifications, also for product-level carbon footprint reports (ISO 14067).

Updated in 2018, ISO 14064 defines 6 categories for carbon emissions within Scope 1-3 (see figure).

The norm focuses on the entire activities of an organization in the context of carbon emissions with no special focus on the emissions caused by transportation.

Source: ISO, Jurić, Ž., & Ljubas, D. (2020)

¶ ISO 14068

ISO 14068 is the specification on Greenhouse gas management, climate change management, and related activities — Carbon neutrality. Currently under development, the standard aims to provide a harmonized approach to achieving carbon neutrality and communicating any associated claims. Companies following the guidelines in this standard would be able to claim carbon neutrality.

Among the benchmark standards and methodologies on carbon neutrality are the Carbon Neutral Protocol, developed in the United States by Natural Capital Partners, and the PAS 2060 ‘Specification for the demonstration of carbon neutrality’ developed in the United Kingdom.

Source: ISO, Ecostandard

¶ ISO 14083

ISO 14083 deals with the 'quantification and reporting of greenhouse gas emissions arising from operations of transport chains'. The new leading standard for all emissions quantifications within the transport sector replaced EN16258 and was developed in collaboration with the Smart Freight Centre and the GLEC framework. ISO 14083 is proposed to be the new mythological calculation basis for the upcoming “CountEmissions EU” initiative, which would mean that all companies reporting their emissions under this initiative must comply with it. It covers all relevant modes and means of modern-day transport chains.

ISO 14083 considers the full transport chain for freight and passengers and thus all possible sources of emissions that could be emitted during the transport, storage and handling of the transported goods. This includes both transport and hub-related emissions.

It introduces the concept of clustering transport activities within the transport chain, that share the same emissions intensities, into so-called transport and hub operations categories (TOCs and HOCs). This facilitates the detailed reporting of emissions but also enables comparison and benchmarking of emissions calculations within and outside of the organization. It provides guidance for the calculations of scopes 2 and 3 emissions and provides default values for fuel emissions (separated into WTW, TTW, and WTT), empty and load factors of vehicles, default intensities and many more relevant default values.

It moreover, expanded the scope of the emissions calculations among others to leaked refrigerants, start-up and idling of vehicles and also included support IT activities and emissions caused by repackaging on a voluntary basis. Carbon offsetting, produced waste, co-located businesses in the hub and the maintenance and construction of equipment and transport infrastructure are still excluded from the calculations. More detailed information about the new ISO 14083 can be found in our blog post (ISO 14083 Blogpost).

Source: ISO

¶ MARPOL

The International Convention for the Prevention of Pollution from Ships (MARPOL) is the main international convention to prevent pollution of the marine environment by ships. It was adopted in 1973, entered into force in 1978, and was subsequentially updated.

The first Annex in 1983 regulates the prevention of pollution by oil, followed by regulations for control of pollution by NOx in bulk in 1987, the prevention of pollution by garbage or sewage from ships in 1998 and 2003, and regulations concerning harmful substances carried at sea in packaged form in 1992. The latest annex added regulations to prevent air pollution from ships.

Source. IMO

¶ PAS 2060

PAS 2060 is a specification developed by the British Standards Institution. It defines a consistent set of measures and requirements for entities (e.g. organisations, governments, or individuals) to demonstrate carbon neutrality for a product, service, organisation, community, event, or building.

The carbon footprint measurements should include 100% of Scope 1 & 2 emissions, and Scope 3 which contribute more than 1% of the total footprint.

The entity must develop a Carbon Management Plan which contains a public commitment to carbon neutrality and outlines the reduction strategy: a time scale, specific targets for reductions, the planned means, and how residual emissions will be offset.

PAS 2060 requires that the total amount of carbon emissions at the end of a reduction period be offset by high-quality, certified carbon credits: approved by PAS schemes, verified by an independent third party, and confirmed by a credible registry.

The PAS 2060 standard specifies a four-stage process to demonstrate carbon neutrality. This involves:

- Assessment of GHG emissions based on accurate measurement data

- Reduction of emissions through a target-driven carbon management plan

- Offsetting excess emissions, often by purchasing carbon credits

- Documentation and verification through qualifying explanatory statements and public disclosure.

Source: BSI, wiki, carbon-clear.com

¶ Pathfinder Framework

Pathfinder Framework is a guide for calculating and exchanging of product-level carbon emissions' data across value chains, including quality assurance and verification schemes for data comparability and reliability. Published in June 2021 by the Carbon Transparency Partnership (CTP), it represents the efforts of 35+ companies, standard-setting bodies, and industry initiatives and aims to improve the data transparency for product carbon footprint.

The following topics are covered in the first version of the guidance:

Guidelines for accounting of Product Carbon Footprints

- Hierarchy of application of existing product standards and methods

- Unification of relevant approaches

- Hierarchy of data types with prioritization logic for use of primary data

- Approach to secondary data usage

- Calculation process for determination

Guidelines for exchange of Product Carbon Footprints

- Minimum required data elements for exchange

- Data quality requirements for PCF data

- Scope and process for verification of PCF data.

In the next version of the Pathfinder Framework specific guidelines for the tech-enabled exchange of PCF are expected.

In addition to the framework, the CTP is developing a Pathfinder Network to bring together different solutions and platforms, with the objective of enabling different supply chain actors to have access to the primary emissions data associated with their products.

Sources: Carbon Transparency Partnership, Pathfinder Framework, Pathfinder Network

¶ UNFCCC

UNFCCC is a United Nations Framework Convention on Climate Change aimed at the prevention of “dangerous” human interference with the climate system. It is an international environmental treaty, also called as ‘Rio Convention’ negotiated at the United Nations Conference on Environment and Development (UNCED) in Rio de Janeiro in 1992.

It entered into force in March 1994. The Convention has near universal membership (198 Parties) and is the parent treaty of the 2015 Paris Agreement. The UNFCCC is also the parent treaty of the 1997 Kyoto Protocol.

The ultimate objective of all three agreements under the UNFCCC is to stabilize greenhouse gas concentrations in the atmosphere at a level that will prevent dangerous human interference with the climate system, in a time frame that allows ecosystems to adapt naturally and enables sustainable development.

Source: UNFCCC

¶ Ro-Ro GHG Emissions Accounting Guidance

Roll-On Roll-Off (Ro-Ro's) are a special category of maritime logistics and thus need more specific reporting guidance. In 2023 the SFC (Smart Freight Centre) and the ECG (Association of European Vehicle Logistics) published a methodology for the harmonization of GHG quantification measures specifically for the Roll-On Roll-Off (Ro-Ro) segment. The methodology aimed to address the current challenges of Ro-Ro GHG emission quantifications, due to their specific route, capacity, and task design, by adding more details to the methodology already provided by ISO14083. They identified and created a mass-independent measurement unit for Ro-Ro's and agreed on more detailed reporting from 2025 (for more information see SFC).

¶ Fraunhofer Institute for Material Flow and Logistics (Fraunhofer IML)

The Fraunhofer Institute for Material Flow and Logistics (Fraunhofer IML) focuses on warehouses, transhipment sites and distribution centre's and the resulting GHG emissions that are caused by them within the transport chain. Emission factors for various activities within these facilities, such as storage and transhipment in various temperatures are determined with the help of industry collaboration. The Fraunhofer IML is part of the international GILA project, which also includes the Politecnico di Milano, GreenRouter and Universidad de los Andes. The IML publishes their reports and default values annually.

¶ Green Freight Programs

¶

Clean Cargo

Clean Cargo is the cargo shipping industry’s leading buyer-supplier forum for sustainability. Its members represent 85% of global container cargo capacity. Clean Cargo provides a methodology for CO2 emissions calculations that has become a global standard in the ocean container shipping sector. Besides measuring and evaluating performance data, it supports collaborative projects that drive improves sustainability performances and organizes bi-annual meetings to share best practices and enhance corporate engagement in public policy.

Source: Clean Cargo

¶ EcoTransIT World Initiative

EcoTransIT World Initiative (EWI) aims to continuously develop methodologies for the calculation of emissions in the global logistics sector. The EWI is a consortium of industry stakeholders including freight forwarders, shippers, carriers, and research organizations.

EcoTransIT World provides software for calculations of carbon emissions, air pollutants, and external costs. Its calculation logic is among the most used to analyze greenhouse gas emissions in freight transportation. The methodology developed by Infras, Ifeu, and Fraunhofer is accredited by the GLEC framework and meets the requirements of EN 16258 and the GHG protocol.

Source: EWI

¶ Green Freight Asia

Green Freight Asia is a non-profit association of industry players of all sizes that collaborate with NGOs, governments, and industry companies to reduce CO2 emissions and energy consumption by raising energy and fuel efficiency. It offers programs varying from measurement and reporting over carbon offsetting up to labeling and certification.

Source: Green Freight Asia

¶ Lean and Green Europe

Lean and Green is an initiative for businesses and authorities to support sustainable transportation available in 5 European countries. It encourages taking measures for improved environmental sustainability that simultaneously yield cost savings. If an organization can show through an action plan that it will be able to reduce its CO2 emissions by 20% in five years, it becomes eligible for the Lean and Green Award. If the objective in the action plan is fulfilled, the organization is certified by a Lean and Green Star.

Source: Lean and Green

¶ SAFA - Sustainable Air Freight Alliance

The Sustainable Air Freight Alliance (SAFA) is a collaboration between shippers, freight forwarders, and air freight carriers. It concentrates on air freight with the goal of tracking and reducing CO2 emissions and promotes responsible freight transport.

To do so, buyers and suppliers are invited to build dialogue and leverage collective knowledge and action to establish best practices and share innovations for reducing GHG emissions. The initiative is facilitated by BSR, a global nonprofit organization that has more than 250 member companies in its network.

Source. BSR

¶ SmartWay

SmartWay is a voluntary public-private program of the US Environmental Protection Agency that aims to support companies in their ways to more sustainable supply chains by measuring, benchmarking, and improving freight transportation efficiency. For this purpose, it provides a system that tracks, documents, and shares information about fuel use and freight emissions and helps companies in their efforts to improve freight efficiency

Source: EPA

¶ Smart Freight Centre

The Smart Freight Centre is a global non-profit organization with the aim of guiding the global logistics sector towards zero emissions and efficiency and thus contributing to the Paris Agreement.

Here are the key SFC initiatives or where the SFC is present:

- GLEC Framework: widely recognized methods and guidance to decarbonizing logistics

- Sustainable Freight Buyers Alliance: Uniting freight buyers and freight decarbonization initiatives

- Clean Cargo: Decarbonize Marine Transportation

- Air freight: decarbonize air freight, to be launched in 2023

- Smart Freight Alliance China: decarbonize logistics in China

- Smart Freight Alliance India: to be launched

It connects multinational organizations by initiating joint projects, fostering information exchange, and developing global guidelines to report and reduce emissions. Furthermore, the Smart Freight Centre is advocating for industry-wide uptake and government policy alignment. With the GLEC framework, it has developed a comprehensive framework for greenhouse gas emissions calculation and reporting for freight logistics.

Source: Smart Freight Centre

¶ Sustainable Freight Buyers Alliance

The Sustainable Freight Buyers Alliance (SFBA) is an Alliance organized within the Smart Freight Center. It unites freight buyers and freight decarbonization initiatives to shift to zero emissions freight transport.

Three main goals of the SFBA:

1) a common platform for the networking and facilitation of collective projects;

2) a solution hub with the instruments for streamlining information & decarbonizing procurement;

3) tools to track and demonstrate progress for increased visibility in and beyond the logistics sector.

Many brands have committed and joined the SFBA, among the following big brands: Brambles, Cargill, Heineken, HP, Mars, P&G, PepsiCo, Tata Steel, Unilever, Meta, Nike, and UPS.

Source: Smart Freight Center

¶ Regulation

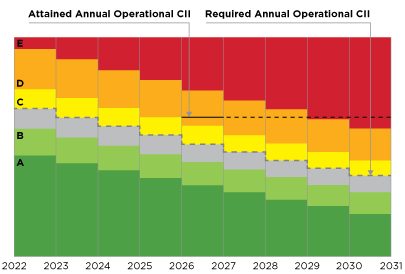

¶ CII - Carbon Intensity Indicator

The Carbon Intensity Indicator (CII) is a measure of how efficiently a ship transports goods or passengers and is given in grams of CO2 emitted per cargo-carrying capacity and nautical mile (see figure). CII was introduced alongside with EEXI as Amendments to the International Convention for the Prevention of Pollution from Ships (MARPOL) Annex VI, which entered into force in November 2022.

The CII applies to all cargo, RoPax, and cruise ships above 5,000 GT, and must be calculated and sent for verification yearly, starting from 2023, in order for a ship owner to receive the Annual Statement of Compliance.

CII is calculated based on reported IMO Data Collection System data and the ship is given a rating from A to E. For ships that achieve a D rating for three consecutive years or an E rating in a single year, a corrective action plan needs to be developed as part of the SEEMP and approved. The rating thresholds will become increasingly stringent towards 2030.

¶ EEDI - Energy Efficiency Design Index

The Energy Efficiency Design Index (EEDI) provides a standard for new ships, assuring that ship designs achieve a certain level of efficiency and decrease carbon emissions. The EEDI is a sister index to EEXI, calculated in the same way (see EEXI) but applied to new ships. The EEDI was introduced by the IMO in 2013 and is well established today in the maritime community.

For most newbuilds, the EEDI is mandatory, i.e. they need a class-approved certificate on EEDI. If a newbuild requires an EEDI or not depends on certain parameters like the ship type, installed engine power, keel laying date, and a lot more. For newbuilds that require an EEDI, shipyards are responsible for the calculation of the EEDI, which is then verified by classification societies. For this purpose, shipyards have to prepare a technical file containing the EEDI calculation.

The following guidelines were developed to support calculation, EEDI certification, and compliance processes (see here).

The EEDI gives owners of ships a competitive advantage. Ships with attained EEDI have a higher probability of winning charter contracts. Furthermore, the European Union has stated its intention to publish the technical efficiency (EEDI or EIV) for each ship that calls at ports in the EU in their recently adopted regulation on Monitoring, Reporting, and Verification (MRV) of emissions from maritime transport (commonly known as the MRV regulation).

Source: IMO

¶ EEXI Energy Efficiency eXisting ship Index

EEXI is an Energy Efficiency eXisting ship Index, introduced by the IMO to reduce the greenhouse gas emissions of ships. The EEXI measures CO2 emissions per transport work (see figure), considering the ship’s design, not operational parameters. Ships must attain EEXI approval (threshold level is defined for ship types and sizes) once in a lifetime, by the first periodical survey in 2023 at the latest.

EEXI regulation applies to ships above 400GT falling under MARPOL Annex VI through a one-time certification.

If the calculated EEXI does not comply with the required EEXI value, changes to the design are needed. This might be the installation of energy efficiency technologies or a limitation of the installed main engine power. The latter is chosen most often. With the restriction of the available propulsion power, the main engine power value applied in the EEXI formula decreases, but at the same time the reference ship speed decreases, and specific fuel oil consumption increases as well.

The following guidelines were developed to support calculation, EEXI certification, and compliance processes:

- MEPC.350(78): EEXI calculation guidelines

- MEPC.351(78): EEXI survey and certification guidelines

- MEPC.335(76): Engine Power Limitation guidelines

Along with the EEXI regulation, the Carbon Intensity Indicator (CII) is coming to force in 2023.

¶ EU Corporate Sustainability Reporting Directive (CSRD)

The Corporate sustainability reporting directive (CSRD) is an EU legislation requiring companies of a certain size operating in the EU to report sustainability information. The policy was designed to support investors, consumers, and other stakeholders evaluating companies’ non-financial performance. The CSRD is to replace the Non-Financial Reporting Directive (NFRD) and is to be realized in several stages for the fiscal years (see also the timeline):

1. 2024 large EU companies previously subject to NFRD

2. 2025 other large EU companies, having two of three criteria: 250 employees, €40 MM turnover, €20 MM assets;

3. 2026 opt-in for listed EU SMEs, two of three criteria 10 employees; €8 M turnover, €4 M assets.

4. 2028 mandatory for listed EU SMEs and non-EU companies (€150 MM turnover in the EU) with at least one EU subsidiary/branch (large or €40 MM turnover in the EU)

It will be mandatory for companies to have their sustainability information assured by qualified third parties, consistent with European Commission standards. The first set of standards is to be adopted by the European Commission by June 2023.

The timeline of the EU’s corporate sustainability reporting regulations as they come into force:

Source: European Council, unipri.org, 2022

¶ EU-MRV

The Monitoring, Reporting, and Verification (MRV) Regulation is an EU legislation entered into force on July 2015. It provides requirements for the monitoring, reporting, and verification of carbon dioxide (CO2) from ships arriving at, within, or departing from EU ports and/or European Economic Area ports.

The MRV Regulation forms part of Europe’s efforts to reduce greenhouse gas emissions and applies to ships above 5'000GT, regardless of flag. The first reporting started in 2018.

Currently, similar types of data must be reported in two separate but overlapping, systems: the EU MRV – which applies since 2018 – and the IMO DCS – which applies since 2019. Below is the table comparing these two systems:

Source: EU Commission, EU Parliament

¶ EU Non-Financial Reporting Directive (NFRD)

The Non-Financial Reporting Directive (2014/95/EU) lays down the rules on disclosure of non-financial and diversity information by large public-interest companies with more than 500 employees. It is applied from 1 Jan 2019 onwards.

The following information must be covered:

- environmental matters

- social matters and treatment of employees

- respect for human rights

- anti-corruption and bribery

- diversity on company boards (in terms of age, gender, educational and professional background)

This directive helps investors, consumers, policymakers, and other stakeholders gauge a company's non-financial performance. Assurance for this reporting is not required.

According to the new EU rules, NFRD is to be replaced by CSRD from the end of the fiscal year 2023, with additional entities, reporting requirements, and assurance to cover.

Source: European Commission, BDO

¶ EU Renewable Energy Directive (RED)

The renewable energy directive (RED) is the legal framework for the development of renewable energy (RE) across all sectors of the EU economy. RED is revised within ‘fit for 55 package’ targeting to cut greenhouse-gas emissions (GHG) by at least 55% in 2030 versus 1990 levels. Introduced in 2008 the RED was revised in 2018 (RED II) and is legally binding since June 2021.

The existing directive – RED II – sets the common EU target to achieve 32% of RE in total energy consumption by 2030. It also includes rules to ensure the uptake of renewables in the transport, heating, and cooling sector, as well as common principles for renewables supporting schemes, the rights to produce and consume RE and to establish RE communities, and sustainability criteria for biomass.

The sub-target for the transport sector is that EU Member States must require fuel suppliers to supply a minimum of 14% of the energy consumed in road and rail transport by 2030 as RE. The RED II also defines a series of sustainability criteria that bioliquids used in transport must comply with to be counted towards that goal and be eligible for financial support by public authorities. There is a dedicated target for advanced biofuels produced from feedstocks. The contribution of advanced biofuels and biogas produced from the feedstock shall be at least 0,2 % in 2022, at least 1 % in 2025, and at least 3,5 % in 2030 of total energy consumption in the transport sector.

The recently approved RED III increased those targets further by demanding a binding target of 42.5% share of renewable energies. For the transport sector, the shares have increased from 14% of renewable energy sources to 29% and from 3.5% to 5.5% for used biofuels (RED III).

Sources: EU Commission, KPMG

¶ EU Sustainable Finance Disclosure Regulation (SFDR)

The Sustainable Finance Disclosure Regulation (SFDR) is a European regulation introduced to improve transparency in the financial services sector and help investors consider the environmental and/or social characteristics of financial products. It came into force in March 2021.

The scope of the EU SFDR applies to all financial market participants such as banks, insurers, asset managers, and advisers based in the EU or outside of the EU if they market their products to EU clients.

The EU SFDR requires specific firm-level reporting from asset managers and investment advisers on two key considerations:

- Sustainability Risks - environmental, social, or governance events which could cause a material negative impact on the value of an investment;

- Principal Adverse Impacts - any negative effects that investment decisions or advice could have on sustainability factors (carbon dioxide emissions, poor water, waste, or land management practices).

Larger firms (having more than 500 employees) are required to disclose how they consider Principal Adverse Impacts from 30 June 2021. The SFDR’s regulatory technical standard will come into effect on January 1st, 2023.

¶ EU Taxonomy

Implemented as a part of the EU Green Deal initiatives, the EU taxonomy is an EU regulation that establishes a classification system to evaluate economic activities, and define when a company is operating sustainably or environmentally friendly. The aim of the EU Taxonomy is to direct capital flows into ecologically sustainable activities. In essence, the EU Taxonomy provides ways through which a company can calculate its sustainability turnover.

The Taxonomy Regulation entered into force on 12 July 2020 with the first reporting for related companies after 31 December 2021.

Under the EU Taxonomy Regulation an economic activity must substantially contribute to one of six environmental aims:

1. climate change mitigation;

2. climate change adaptation;

3. sustainable use and protection of water and marine resources;

4. transition to a circular economy;

5. pollution prevention and control;

6. protection and restoration of biodiversity and ecosystems.

It must also meet minimum social OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights.

For environmental disclosure purposes, the EU Taxonomy is reflected in Non-Financial Reporting Directive NFRD (soon to be replaced by Corporate Sustainability Reporting Directive) and the Sustainable Finance Disclosure Regulation SFDR.

Under CSRD, non-financial companies will have to report the percentage of their Taxonomy-aligned turnover, CAPEX, and OPEX (environmental performance is to be translated into financial variables).

Under SFDR financial, companies must report to what extent it uses the EU Taxonomy, what environmental objectives their investments contribute, and the percentage of Taxonomy-aligned economic activities in their financial activities, such as lending, investment, and insurance.

Sources: EU commission, JP Morgan

¶ IMO DCS

The International Maritime Organization (IMO) adopted a mandatory Fuel Oil Data Collection System (DCS) for international shipping, requiring ships of 5'000 gross tonnage or above to start collecting and reporting data to an IMO database from 2019.

It was adopted on 28th October 2016 as amendments to Chapter 4 of Annex VI of MARPOL.

What does it mean for ship owners and ship operators:

Ships of 5’000 GT and above have to submit annual reports on fuel consumption, distance travelled and hours underway to their Administration;

Aggregated data will be reported to a ship’s flag State after the end of each calendar year, which will need to verify that the data has been reported in accordance with the requirements before issuing a Statement of Compliance to the ship.

IMO DCS is overlapping with EU MRV, see details under the EU MRV.

Source: IMO

¶ Lieferkettengesetz

The Lieferkettengesetz (Gesetz über die unternehmerischen Sorgfaltspflichten in Lieferketten) or the German Supply Chain Due Diligence Act (GSCA) requires companies to assess human rights and environmental risks across their entire supply chain. It combines various German laws with the intent to eliminate child labor, ameliorate poor labor working conditions, and provide certain environmental protections within global supply chain activities.

The Supply Chain Act takes effect from 1 Jan 2023 and is applied to all companies with 3,000 employees or more, whose head office, main branch, or statutory seat is in Germany. Starting in 2024, the scope is extended to companies with more than 1,000 employees. In violation of GSCA, a company can be required to pay fines of up to 2% of its annual revenue.

The Act applies to all organization’s direct and indirect suppliers (not necessarily based in Germany), from the extraction of the relevant raw materials through to the delivery to the end customer.

To fulfill the requirements of the GSCA and ensure vendors are as compliant as possible, organizations should conduct human rights and environmental due diligence using the following framework:

- Establish a Supply Chain risk analysis and risk management system

- Develop a human rights’ and associated environmental strategy for a company supply chain

- Impose certain obligations on direct (first-tier) suppliers

- Create Measures for Lower-tier Suppliers

- Report Annually on Compliance with Due Diligence Obligations

CSCA has connection points to the environmental sustainability of supply chains but is not taking this particular issue into the focus of the legislation. Therefore precise metrics of emissions caused by tier-1 to tier-n suppliers from the logistics network are not at the core of this regulation.

Source: Bundestag, Supporting documents, Exiger

¶ SEEMP - Ship Energy Efficiency Management Plan

The Ship Energy Efficiency Management Plan (SEEMP) is an operational measure that establishes a mechanism to improve the energy efficiency of a ship in a cost-effective manner. The SEEMP was made mandatory by the Marine Environment Protection Committee (MEPC) for all ships with the adoption of amendments to MARPOL (The International Convention for the Prevention of Pollution from Ships), Annex VI. These amendments are considered by the maritime industry as the first legally binding climate change treaty to be adopted since the Kyoto Protocol.

The SEEMP also provides an approach for shipping companies to manage ship and fleet efficiency performance over time using, for example, the Energy Efficiency Operational Indicator (EEOI) as a monitoring tool. The guidance on the development of the SEEMP for new and existing ships incorporates best practices for fuel-efficient ship operation, as well as guidelines for voluntary use of the EEOI for new and existing ships.

Currently, three parts of the SEEMP exist:

SEEMP Part I, effective from Jan 2013, is a ship management plan to improve energy efficiency, mandatory for all ships of 400 GT or above. Content is not subject to verification.